Forward workplan for systemic reviews 2024/25

Forward work plan for systemic reviews 2024/25

About our work plan

One of the core statutory functions of the Inspector-General of Taxation and Taxation Ombudsman (IGTO) is to:

“improve the fairness and integrity of the taxation and superannuation administration through review investigations of systemic and broader community issues, reporting issues that are in the public interest and independent advice to the Government and its relevant entities.”

The IGTO aims to complete four systemic reviews per year. Stakeholders from across the community, government and tax profession will be invited to contribute to each review.

Our work plan sets out the areas that we have identified as suitable for broad, systemic reviews for the 2024-25 financial year. There are two types of reviews that we may undertake:

- issues reviews which seek to address specific issues of concern that have been identified; or

- assurance reviews which examine key topic areas with a view to providing assurance to the Government and broader community about the Australian Taxation Office (ATO)’s administration of those areas.

The topics have been identified following comprehensive research, analysis and consultation that have included examination of:

In mid-September 2024, we issued our draft work plan for consultation. We have consulted with a range of stakeholders about the topics identified in the draft work plan. These stakeholders included:

- Parliament and Government

- Assistant Treasurer

- Parliamentary committees

- Public sector

- Australian Taxation Office

- Tax Practitioners Board

- The Treasury

- Australian National Audit Office

- Commonwealth Ombudsman

- Australian Small Business and Family Enterprise Ombudsman

- Private sector/not-for-profit organisations

- Tax professional and industry bodies

- Community organisations

- Academics

The purpose of the consultation was to ensure that we identified topics that are most important and likely to be of the highest impact to the broadest segments of the community.

Ultimately, the issues included in the work plan are those determined by the IGTO to be most relevant and impactful.

This work plan is divided into two sections:

- Short list priority areas for review which are topics we will review in 2024–25

- Other topics that were the subject of consultation but ultimately not selected for review during this cycle.

Other ways we may address issues

The work plan sets out topics that we have selected for reviews under the powers defined within our legislation. Such reviews are not the only option available to us to surface issues, encourage public discourse and identify opportunities for improvement. We will continue to monitor the issues that have not been selected for review and, where appropriate, consider options to explore those issues further through other means. Some of these options include:

- direct engagement with relevant Commonwealth agencies;

- advice to Government;

- contributions to public policy debates;

- submissions to other Parliamentary and government consultations or inquiries;

- input to the work of partner organisations; and

- thought leadership articles.

Next consultation

The work plan is not a fixed document. We will consult with stakeholders to refresh and update our work plan every six months to ensure that it remains relevant and responsive to changing environmental, social and policy priorities. The next consultation of the work plan will be undertaken in May 2025.

Our work plan at a glance

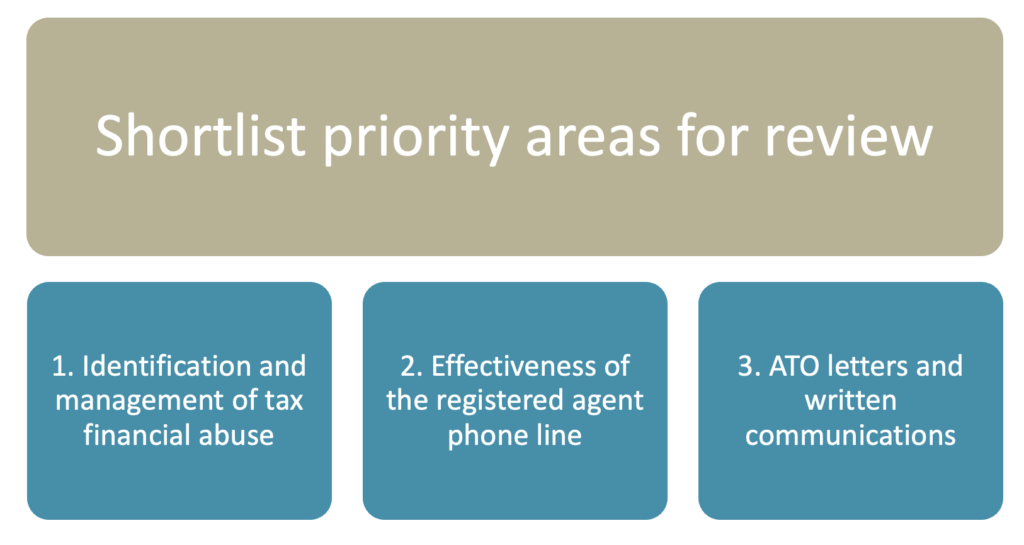

Shortlisted Priority Areas for Review

Issues review: identification and management of tax financial abuse

Financial abuse is a form of family and domestic violence. It may manifest in a number of ways. In the tax system, it can result in one partner or another family member unwittingly becoming liable for tax debts related to entities over which they have no or limited control.

A range of initiatives are currently under way across government and within industry to combat financial abuse and improve support for victim-survivors of family and domestic violence. A current example is the Parliamentary Joint Committee on Corporations and Financial Services’ inquiry to examine the role of financial institutions in identifying and preventing financial abuse, the effectiveness of existing laws to govern the ability of banks to deal with financial abuse, and potential areas for reform.

Our review is not intended to replicate prior or existing work in this important area. Rather, it aims to contribute to and support broader Parliamentary, academic and community efforts to combat financial abuse by examining the issue through the lens of ATO policies and procedures.

There are presently limited options in the tax law for the ATO to directly deal with tax financial abuse and support victim-survivors. As the ATO increases its efforts to reduce the current balance of undisputed, uncollected debts, it is critical that there are effective processes and procedures for dealing with liabilities that were not genuinely or legitimately incurred by the taxpayer.

Our review will focus on the ATO’s processes for identifying instances of tax financial abuse, the support that it is able to offer to victim-survivors, and whether the tax law provides sufficient powers for the Commissioner to grant relief where tax financial abuse is demonstrated.

We will engage with the full range of stakeholders in government, academia, community organisations, and industry to scope and progress this review, including all those who have contributed substantive research, policy, and advocacy work already.

The review would examine:

- the ATO policies and procedures for identifying and supporting victim survivors of tax financial abuse (including through financial hardship relief channels);

- how ATO leverages the input and insight of other agencies with relevant specialist expertise and experience;

- whether the tax law currently provides sufficient powers for the Commissioner to grant relief where tax financial abuse is demonstrated; and

- whether the ATO has robust and effective policies in place to identify and hold perpetrators of financial abuse to account (including in collaboration with other agencies).

Issues review: effectiveness of the registered agent phone line

Registered tax and business activity statement agents (collectively, registered agents) play a critical role in the effective administration of tax and superannuation. They represent and assist more than 70% of individual taxpayers and more than 90% of businesses to effectively manage their tax affairs.

The efficient and effective engagement between the ATO and registered agents is therefore essential to the health and efficient administration of the tax system. Amongst other engagement channels, the ATO maintains a dedicated registered agent phone line to assist agents in their day-to-day work. The IGTO has received concerns about the timeliness and effectiveness of engagements through the registered agent phone line, capacity and capability of ATO staff who manage the phone line and the level of support and assistance to troubleshoot issues relating to the recently implemented client-agent linking system.

In our consultations to date, we have identified a mismatch of expectations between what agents want from the ATO’s dedicated phone line, and the service offer from the ATO. Exploring expectations will help understand what causes misunderstandings or frustrations in the agent community and ATO.

We note that as part of the 2022-23 audit of the ATO’s engagement with tax practitioners, the Australian National Audit Office (ANAO) examined the registered agent phone line and recommended that the ATO ‘consult with tax practitioners to better understand their concerns regarding the registered agent phone line and use this feedback to guide the development of future service offerings’. In this review, we will seek to understand how the ATO has progressed with its implementation of the ANAO recommendation.

The review would examine:

- the timeliness of responses to calls made to the registered agent phone line;

- whether the resourcing and capability of the officers assigned to the registered agent phone line are adequate and sufficient to meet agent demands and expectations; and

- opportunities to improve the effectiveness of the registered agent phone line to support agents.

Assurance review: ATO letters and written communications

Voluntary compliance relies on taxpayers understanding what is required of them from the tax office. The ATO engages with the Australian community through various types of communications. A significant proportion of these communications occur in the form of letters.

Good written communication creates certainty, minimises confusion and fosters confidence in interactions. It is also likely to generate the intended responses from the community. Conversely, poor communication creates a cost to the ATO – from the volume of calls, enquiries, complaints received and non-compliance/disengagement from the tax system.

It is therefore critical that the ATO ensures that it designs and writes its letters in a style and language that sufficiently enables taxpayers to understand what is being asked of them as well as their rights and obligations.

Through a sample of major batch communication letters issued over the last 12 months, we would examine how the ATO designs and tests its written communications, processes in place to address any confusion or uncertainty arising from the content of communications, and how feedback is received and used to improve letter design and written communications.

The review would examine:

- the ATO’s processes for designing and testing letters and written communications;

- the adequacy of its processes for addressing any confusion or uncertainty arising from the content of communications, and receiving and evaluating feedback to improve the design, layout and content of letters; and

- opportunities for the ATO to improve its written communication to taxpayers.

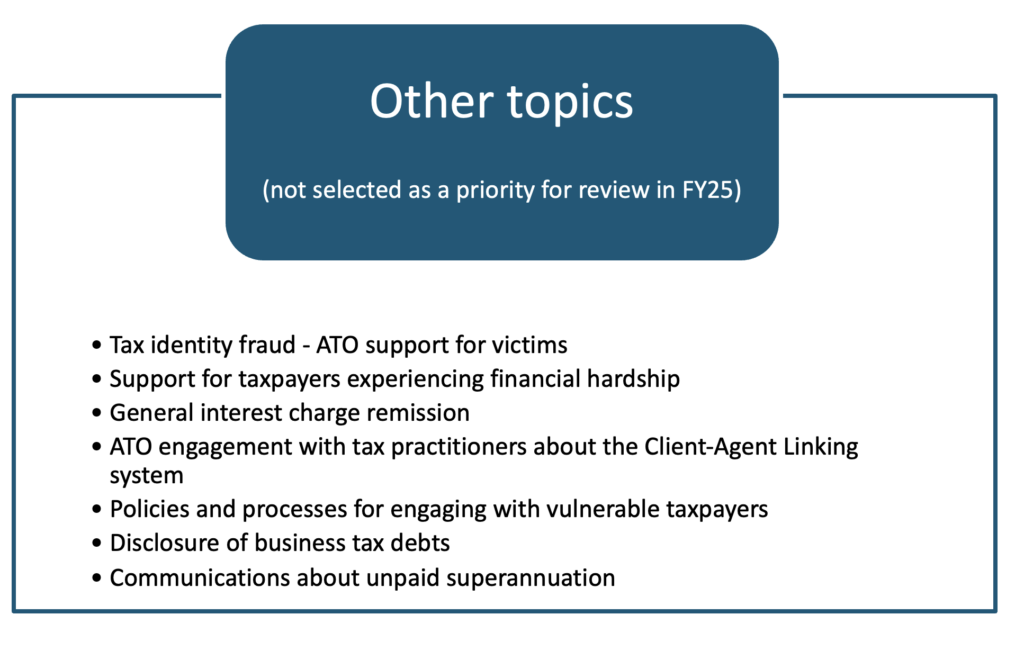

Other Topics

As part of our consultations on the draft work plan, we sought feedback on a range of other topics. Due to our limited review resources, it is not possible for us to review every topic brought to our attention. We have briefly set out below why we have not been able to shortlist those topics for the 2024-25 work plan. Topics that have not been selected remain on our list of potential review topics.

We will consult with stakeholders again in May 2025 in relation to these topics and any other emerging topics as part of our work plan refresh.

Issues review: tax identity fraud – ATO support for victims

This topic received strong support and interest. However, stakeholders did not provide a consensus on timing of the review, noting the risk of overlap and issues being overtaken by work concurrently under way.

The ATO has also been updating its processes following phase 1 of the IGTO’s own initiative investigation into tax identity fraud. We will be following up the ATO’s agreement and implementation plans for the recommendations made in the interim report. We have therefore determined that a review on this topic after FY25 would likely yield more meaningful improvements once other work and improvements have been completed.

Assurance review: support for taxpayers experiencing financial hardship

This topic received strong support from stakeholders given the current context of “cost of living” pressures within the community. But many stakeholders also acknowledged potential overlaps with other programs of work within the Government. Financial hardship is a broad area that has many underlying causes, one of which may be due to financial abuse. Accordingly, we propose to explore an element of financial hardship within the identification and management of tax financial abuse review. As ATO debt management actions continue to ramp up, we will return to the issue of hardship in 2025/6.

Issues review: ATO engagement with tax practitioners about the Client-Agent Linking system

This topic remains on our list of potential review topics noting that it has received general support from stakeholders. We note that the Client-Agent Linking system has not yet been fully implemented and some aspects of ATO consultation are still continuing. An aspect of the Client-Agent Linking system (i.e., ATO support for registered tax practitioners and their clients) will be examined as part of the review into the effectiveness of the registered agent phone line.

Assurance review: policies and processes for engaging with taxpayers experiencing vulnerabilities

This topic remains on our list of potential review topics, noting that it has received general support from stakeholders. Vulnerability is a broad topic and may emerge in a number of different contexts.

We understand that the ATO has kicked off a taskforce and program of work on how they support taxpayers experiencing vulnerability. We believe that it would be best to allow these plans to be developed and for us to return to the subject matter once those plans are in train and could be included within our review.

As part of our review examining the ATO’s letters and written communications, we will consider opportunities for the ATO to improve its communications with taxpayers that may experience difficulties.

Assurance review: disclosure of business tax debts

This topic remains on our list of potential review topics noting that it has received general support from stakeholders. We note that from a complaints perspective, the levels of concern about disclosure of business tax debts have not been high.

Issues review: general interest charge remission

This topic remains on our list of potential review topics noting that it has received general support from stakeholders. It also has an overlap with hardship, which will remain high on our list for 2025/6. We continue to address individual taxpayer concerns about GIC remission through our complaints investigation service.

Issues review: communications about unpaid superannuation

We received stakeholder feedback and acknowledge that the Payday Super regime is due to commence from 1 July 2026. It was suggested that a review of this topic may produce more meaningful outcomes following implementation of Payday Super. In the meantime, we will explore other options to bring current, extant issues to the attention of senior executives within the ATO and Treasury through our direct engagement and broader consultation.